Blab Business

BKV Corp: Carbon Capture Upside Dwarfed by Share Dilution, Analyst Rates Hold

BKV Corp’s stock has surged 18.81% over the past year, drawing the eye of investors eager for a foothold in the upstream energy sector. Yet a recent Seeking Alpha contributor cautions that the company’s promising carbon‑capture prospects are being eroded by a persistent risk of share dilution, prompting a Hold rating.

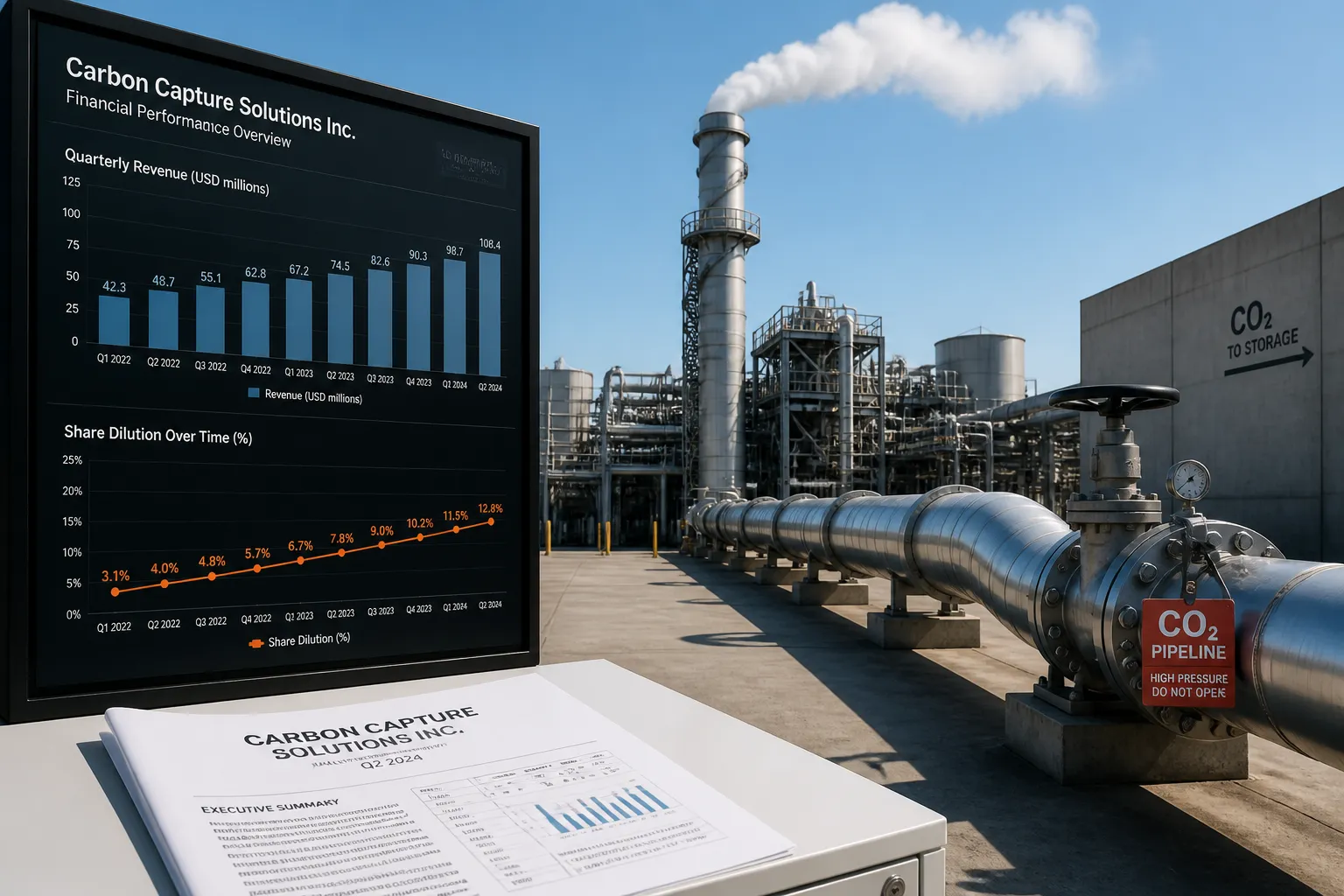

In its Q1 2026 earnings release, dated May 7 2026, BKV reported net income of $44.1 million, translating to $0.42 per diluted share. The report emphasized that natural gas remains the core revenue driver and highlighted that recent acquisitions have broadened BKV’s upstream portfolio, increasing its exposure to commodity price swings.

Share dilution has surfaced as a recurring theme for BKV. DilutionWatch assigns the company a score of 43 out of 100, indicating medium‑to‑high dilution risk. The same source notes that a March 2026 share offering raised capital but also raised concerns about the impact on shareholder ownership. When dilution is factored into earnings projections, the analyst’s model shows BKV’s estimated EPS for fiscal year 2029 falling from $3.59 to $1.93.

Carbon capture and utilization remain a cornerstone of BKV’s long‑term strategy. The company has publicly committed to a net‑zero emissions target for the 2030s and identified CCUS as a significant growth area. According to the Seeking Alpha article, BKV’s CCUS projects aim to capture CO₂ from natural‑gas processing and inject it into enhanced‑oil‑recovery operations. While the potential upside is acknowledged, the analyst stresses that the current dilution risk outweighs the projected long‑term earnings benefits.

BKV’s upstream acquisitions have also influenced its recent performance. The Q1 2026 release highlighted that the acquisitions increased upstream production assets, thereby heightening the company’s sensitivity to natural‑gas prices. This expansion aligns with BKV’s broader strategy to strengthen its position in the upstream sector, traditionally the most volatile segment of the energy industry.

The analyst’s recommendation of Hold reflects a balance between the company’s solid earnings base and its exposure to dilution. The rating is supported by the fact that BKV’s current EPS remains positive, but the projected dilution‑adjusted EPS for 2029 is significantly lower than the undiluted estimate.

Looking ahead, BKV’s next earnings announcement is scheduled for the second quarter of 2026. Investors will likely focus on how the company manages its capital structure, the progress of its CCUS projects, and the performance of its newly acquired upstream assets. The ongoing share‑dilution risk will remain a key factor for analysts and shareholders alike.

In summary, BKV Corp’s share price has risen sharply, driven by a stable earnings base and expansion in upstream operations. Nonetheless, the company’s share‑dilution risk, highlighted by recent analyst commentary, has tempered enthusiasm for its long‑term growth prospects, particularly in the CCUS arena. The Hold rating signals that investors should weigh the dilution risk against the potential upside from carbon‑capture initiatives and upstream expansion.

In its Q1 2026 earnings release, dated May 7 2026, BKV reported net income of $44.1 million, translating to $0.42 per diluted share. The report emphasized that natural gas remains the core revenue driver and highlighted that recent acquisitions have broadened BKV’s upstream portfolio, increasing its exposure to commodity price swings.

Share dilution has surfaced as a recurring theme for BKV. DilutionWatch assigns the company a score of 43 out of 100, indicating medium‑to‑high dilution risk. The same source notes that a March 2026 share offering raised capital but also raised concerns about the impact on shareholder ownership. When dilution is factored into earnings projections, the analyst’s model shows BKV’s estimated EPS for fiscal year 2029 falling from $3.59 to $1.93.

Carbon capture and utilization remain a cornerstone of BKV’s long‑term strategy. The company has publicly committed to a net‑zero emissions target for the 2030s and identified CCUS as a significant growth area. According to the Seeking Alpha article, BKV’s CCUS projects aim to capture CO₂ from natural‑gas processing and inject it into enhanced‑oil‑recovery operations. While the potential upside is acknowledged, the analyst stresses that the current dilution risk outweighs the projected long‑term earnings benefits.

BKV’s upstream acquisitions have also influenced its recent performance. The Q1 2026 release highlighted that the acquisitions increased upstream production assets, thereby heightening the company’s sensitivity to natural‑gas prices. This expansion aligns with BKV’s broader strategy to strengthen its position in the upstream sector, traditionally the most volatile segment of the energy industry.

The analyst’s recommendation of Hold reflects a balance between the company’s solid earnings base and its exposure to dilution. The rating is supported by the fact that BKV’s current EPS remains positive, but the projected dilution‑adjusted EPS for 2029 is significantly lower than the undiluted estimate.

Looking ahead, BKV’s next earnings announcement is scheduled for the second quarter of 2026. Investors will likely focus on how the company manages its capital structure, the progress of its CCUS projects, and the performance of its newly acquired upstream assets. The ongoing share‑dilution risk will remain a key factor for analysts and shareholders alike.

In summary, BKV Corp’s share price has risen sharply, driven by a stable earnings base and expansion in upstream operations. Nonetheless, the company’s share‑dilution risk, highlighted by recent analyst commentary, has tempered enthusiasm for its long‑term growth prospects, particularly in the CCUS arena. The Hold rating signals that investors should weigh the dilution risk against the potential upside from carbon‑capture initiatives and upstream expansion.